Is 6 percent interest rate good for a house?

In today's market, a good mortgage interest rate can fall in the high-6% range, depending on several factors, such as the type of mortgage, loan term, and individual financial circ*mstances. To understand what a favorable mortgage rate looks like for you, get quotes from a few different lenders and compare them.

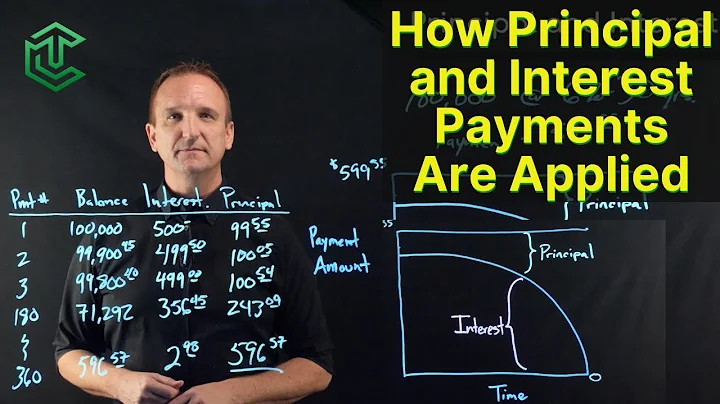

Higher interest rates generally reduce the amount of money you can borrow, and lower interest rates increase it. If the interest rate on our $100,000 mortgage is 6%, the combined principal and interest monthly payment on a 30-year mortgage would be about $599.55—$500 interest + $99.55 principal.

| Loan Type | Purchase | Refinance |

|---|---|---|

| 30-Year Fixed | 7.29% | 7.51% |

| FHA 30-Year Fixed | 7.21% | 7.54% |

| VA 30-Year Fixed | 6.86% | 7.37% |

| Jumbo 30-Year Fixed | 7.07% | 7.08% |

If rates drop even lower — below 5% — nearly one-third of potential buyers say they could afford to buy. Since 2022, when the Federal Reserve began its campaign of interest rate hikes to tame inflation, mortgage rates have been climbing upward with little respite. Two years later, rates stand at almost 6.77%.

A high-yield savings account that pays 5% interest is highly competitive. Not only does it significantly outpace the average savings account interest rate, but it's on the high end of the scale even for high-yield savings products.

As mortgage rates inch lower towards the 6% mark, the real estate market is cooling. Still, many homeowners still have low interest rates compared to the 6.66% they fell to last week. In fact, nearly 89% of borrowers have an interest rate below 6%, a Redfin study reports.

The advertised rate, or nominal interest rate, is used when calculating the interest expense on your loan. For example, if you were considering a mortgage loan for $200,000 with a 6% interest rate, your annual interest expense would amount to $12,000, or a monthly payment of $1,000.

The range of 3% to 6% is hypothetical, but it's not far out of line with the way actual rates have changed in recent years. In January 2021, Freddie Mac reported an average interest rate of 2.65% on a 30-year fixed-rate mortgage. By August 2022, that same mortgage averaged 5.55%.

| FICO Score | National average mortgage APR |

|---|---|

| 660 to 679 | 7.291% |

| 680 to 699 | 7.077% |

| 700 to 759 | 6.900% |

| 760 to 850 | 6.678% |

No one likes it when interest rates go up, but it's not the end of the world. This is still a great time to buy a house—you'll just pay more than you would've a couple years ago. It's also a good time to sell a house. And if you already have a fixed-rate mortgage locked in, you're in good shape too.

Is 7 mortgage rate high?

Here's why 7% mortgage rates are so much worse for buyers now than 20 years ago. Mortgage rates haven't been this high for over two decades, but it's far worse to be a homebuyer now than then. Buyers are still sticker-shocked by the memory of historically low rates when they could afford so much more two years ago.

The monthly income rule

"You want to make sure that your monthly mortgage is no more than 28% of your gross monthly income," says Reyes. So if you bring home $5,000 per month (before taxes), your monthly mortgage payment should be no more than $1,400.

Consumers are mentally anchored to low rates.

66% of those consumers believe a historically “normal” mortgage rate is below 5.5%. Mortgage rates stayed below 5% for 12 straight years, when most of these borrowers bought or refinanced. According to our survey, 90% of current borrowers have a rate below 5.5%.

In today's market, a good mortgage interest rate can fall in the high-6% range, depending on several factors, such as the type of mortgage, loan term, and individual financial circ*mstances. To understand what a favorable mortgage rate looks like for you, get quotes from a few different lenders and compare them.

If the interest rate on your debt is 6% or greater, you should generally pay down debt before investing additional dollars toward retirement. This guideline assumes that you've already put away some emergency savings, you've fully captured any employer match, and you've paid off any credit card debt.

Depending on whether you opt for a 15-year or 30-year mortgage, rates are averaging around 6.5% to 7% — and recently ticked up slightly to a month-long high. And, those types of rates can be a hindrance if you want to buy a new home.

The Fed's latest projections materials show that three rate cuts are still expected in 2024, bringing the rate down by three-quarters of a percentage point by the end of the year.

30-year mortgage rates are currently expected to fall to somewhere between 6.1% and 6.4% in 2024. Instead of waiting for rates to drop, homebuyers should consider buying now and refinancing later to avoid increased competition next year.

The ESR Group expects mortgage rates to decline in 2024, ending the year below 6 percent. The lower rate environment is expected to boost refinance volumes, which are already on the upswing, as evidenced by the recent uptick in Fannie Mae's Refinance Application-Level Index, to nearly double their 2023 levels in 2024.

Your lender can't add the amount of interest above 6 percent back into the loan later on after you leave active duty. You can request an interest rate reduction from your lender at any time while you are serving on active duty and up to 180 days after release from active duty.

Who pays 6 percent interest?

Digital Federal Credit Union has an account that pays over 6% APY, but you must meet membership requirements to get started. You also won't earn this high interest rate on your entire Digital FCU savings balance. Plenty of savings accounts are available around the U.S. and still offer great rates — over 5% APY.

FPCU is offering a very high 6.00% APY special rate on an 8-month regular share certificate that is available to new members with a $1,000 minimum deposit and $5,000 maximum deposit. The special rate isn't available on jumbo certificates.

Mortgage giant Fannie Mae likewise raised its outlook, now expecting 30-year mortgage rates to be at 6.4 percent by the end of 2024, compared to an earlier forecast of 5.8 percent.

The average 30-year fixed rate reached an all-time record low of 2.65% in January 2021 before surging to 7.79% in October 2023, according to Freddie Mac.